Category: Market

Why Long-Term Investing Pays Off During Market Volatility

By Chad Roope, CFA ®, Chief Investment Officer In times of economic uncertainty, it’s easy for investors to feel uneasy. Whether it’s inflation concerns, political events, or market downturns making headlines, short-term volatility can be unsettling. However, long-term investing strategies have consistently proven to be one of the most effective ways to build wealth and stay on track toward financial goals. Instead of reacting emotionally to market noise, long-term investors benefit from taking a step back and focusing on the bigger picture. Here’s why that mindset can make all the difference. The Stock Market Has Recovered from Every Major Crisis Over the last several decades, the U.S. stock market has faced recessions, geopolitical tensions, inflation spikes, and global pandemics. Despite it all, the market has continued to grow. Investors who stayed committed to their long-term investment strategy have historically been rewarded for their patience. This resilience, explained in the graph below, shows the importance of avoiding knee-jerk reactions and maintaining a diversified portfolio built for the long haul. Timing the Market Can Hurt Long-Term Returns Many investors try to avoid losses by pulling out of the market during downturns. But trying to time the market—even with the best intentions—often results in missed opportunities. Some of the strongest market gains have occurred during periods of high volatility. Missing ev

Lineweaver Wealth Advisors Tariffs Market Commentary for April 3, 2025

Join Chad Roope, CFA®, Chief Investment Officer for Lineweaver Wealth Advisors for an important look into the tariffs announced by the Trump Administration on April 2

2024 Review and 2025 Outlook

By Chad Roope, CFA®, Chief Investment Officer 2024 was a great year for the U.S. economy and equity markets. A strong economy, led by strong labor markets and significant investments in Artificial Intelligence, equated to double digit corporate earnings growth and thereby strong equity market performance. The U.S. was the clear economic leader globally and was why we had a strong overweight to quality, U.S. large-cap stocks all year. This overweight and our focus on active asset allocation, fundamental research and timely trade communications led to solid performance in our client portfolios in 2024, with most of our strategies strongly outperforming their benchmarks. Our proven process and seasoned team of Chartered Financial Analysts stand ready to navigate what is likely to be a dynamic environment in 2025. We think 2025 may prove to be a more volatile year given several uncertainties and rich starting valuation levels, but we think the year should prove to be a solid overall. Below are our key views: We expect U.S. outperformance compared to the rest of the world to continue amid solid economic growth, strong labor markets, lower inflation levels, a supportive Federal Reserve, and the potential for tax cuts and deregulatory policies. We continue to prefer large-cap, high quality U.S. equities as we think this is where the strongest overall earnings growth will continue to be. In fixed income, we are prioritizing higher income, shorter duration exposures t

December Market Commentary

This month we are focusing on the U.S. labor market. While having cooled from its red-hot state, it has settled into a relatively healthy position. Following a month of hiring disruptions due to hurricanes and strikes, businesses added 227,000 jobs in November. However, the uneven nature of recent job growth has led many to question the true health of the labor market. Employment growth in 2024 has been concentrated in a few key sectors, primarily health care and government, which have contributed 41% and 21% of this year’s job gains, respectively. Healthcare’s hiring dominance seems less concerning as the sector is still addressing pandemic-related backlogs. However, employment growth dominated by the public sector, which tends to see increased hiring later in the economic cycle, may be viewed as a warning sign. That said, there are important nuances to consider. Government employment as a sector currently accounts for 14.7% of total payrolls. Of the 21% growth referenced above, 90% has come from state and local levels, which appears less troublesome. Moreover, the sector’s share of payrolls remains below its pre-pandemic (2014 – 2019) average of 15.3%, suggesting its recent outsized growth reflects the continued uneven normalization of the labor market post-pandemic. Outside of these two sectors, sluggish manufacturing activity has been a headwind. Still, some cyclical sectors, including construction, leisure, and transportation, have se

Q4 2023 Commentary and Portfolio Changes

Key Takeaways: We are changing our allocations to slightly overweight U.S. quality stocks, seeking to capitalize on the recent market pullback and position for potential upside surprises in U.S. economic growth and corporate earnings. We are leaning into U.S. high-quality stocks expressing a high-conviction preference for the largest cap stocks in the U.S. that appear to have attractive growth profiles. We plan to decrease our exposure to Europe, moving underweight international Developed Market (DM) stocks due to weakening corporate earnings signals and more pronounced downside vulnerability to potential rising energy prices and geopolitical turmoil. We are underweight bonds and overweight cash and short-term instruments that offer very attractive yields. The ghost of September's past haunted markets once again in 2023 and has carried over. This notoriously weak seasonal period - combined with rising rates and declining liquidity - saw stock and bond prices press lower. The S&P 500 Index, for example, is off its late summer highs by almost 10%, and the Bloomberg U.S. Aggregate Bond Index is down a similar amount from its earlier highs. We are potentially facing an unprecedented third year in a row of bond market losses. Overall, it has been a challenging year for investors with only the largest stocks doing well while most equity and fixed-income styles are flat to down. The “Magnificent 7” stocks in the S&P 500

Market Challenges and the Coming Election

Key Points Challenges include elevated virus transmissions, high unemployment levels, the Presidential election and stretched valuation metrics Monetary and fiscal policy combined with vaccine developments are likely to continue to support risk assets 2020: A Historic Year 2020 will be remembered as the year the coronavirus severely tested the basic freedoms and tenets of capitalism in the United States. The virus has proven to be highly efficient in disrupting many of the daily routines we typically take for granted. Like an engine needs clean oil to operate smoothly, the free movement of people, goods, and capital are key lubricants capitalism needs to operate smoothly. The virus is near-perfect friction to this free movement. As we have witnessed, businesses and education systems have difficulty functioning without free movement. Unfortunately, we have also felt the human tragedy the virus has created with nearly 775,000 deaths globally,5 a number that will sadly go higher. For investors, the result has been some of the largest and fastest swings in financial markets and economic conditions in history. Yet given all this bad news and volatility, the resiliency of our people and the capitalistic economy is truly amazing. In short order, doctors and scientists have developed 8 coronavirus vaccines that are in late-stage trials,1 and many new treatments for COVID-19 are being uncovered rapidly. Central banks and governments globally have also delivered unprecedented reli

Sell in May and Go Away: Two Market Myths to Avoid this Summer

by Jim Lineweaver, CFP®, AIF® There’s an old saying you’ve probably heard that says “Sell in May and Go Away.” But is that good advice? What’s the best thing for you and your investments over the historically slower summer months? The phrase “sell in May and go away” is thought to originate from an old English saying, and it turns out it did have some validity, at least from 1950 to around 2013. During that time, the Dow had an average return of only 0.3% during the May to October period, according to Forbes. But, since 2013 there’s good reason to believe that’s no longer the case. For example, the S&P 500 rose nearly 7% from the beginning of May 2017 through the end of October, according to YCharts. The blue-chip index was up 5% during May through October of 2016 as well. Another common myth is the October Effect, which is the perception that stocks tend to decline during the month of October. Most statistics go against the theory. Some investors may be nervous during October because the dates of some large historical market crashes occurred during this month. But fortunately, this seeming concentration of days is not statistically significant. From a historical perspective, October has marked the end of more bear markets than it has acted as the beginning. We try to help all of our clients keep these things in mind when making decisions, and don’t let these myths cloud their judgment.

Market Outlook 2019

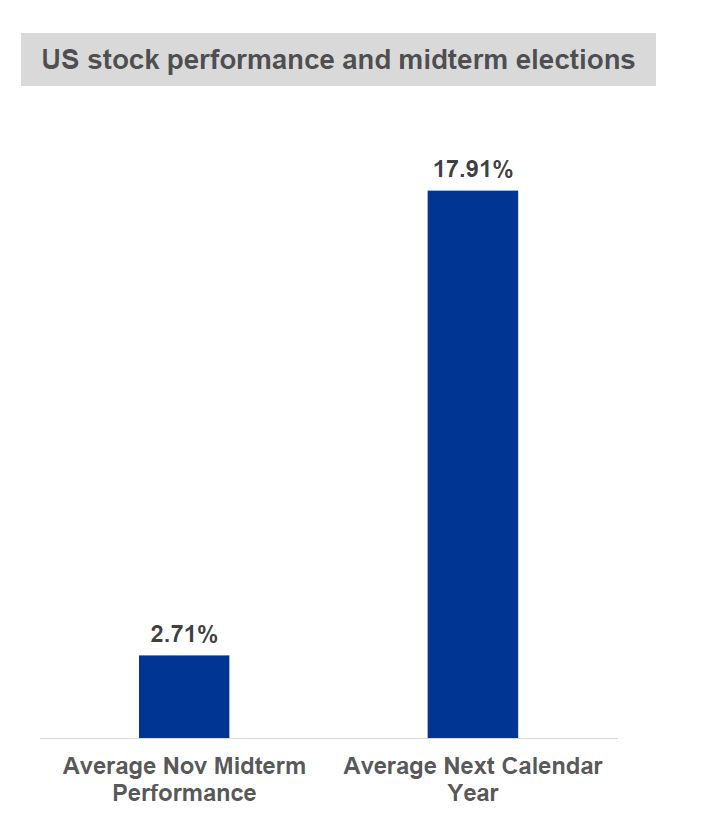

By Chad Roope CFA®, Lead Portfolio Manager - Fundamentum The recent equity market correction has no doubt been uncomfortable. As of the end of year close, the S&P 500 ended the year to date down 6.24%. Concerns about slowing global economic growth, worries that the Federal Reserve is pushing interest rates too far too quickly, fears around the US/China trade war and uncertainties about a US Government shut down have all combined to create downside volatility that we’ve not experienced in a few years. While we agree this is all concerning and that we are likely to continue to see more volatility in the shorter-run, we do not see an economic recession in 2019 based on the data we see today. US corporate earnings growth is likely to be reasonably strong in the first half of 2019, manufacturing data remains in expansionary readings in the US, US unemployment continues to be at historically low levels, and consumer confidence remains relatively high as well. Those are all good signs as well as the fact that many companies are flush with cash, and the recent tax package gives incentives for them to invest this cash in the economy. When taken as a whole, that leads us to believe that the present sell-off is a necessary flushing of the system and growth stocks that may have gotten a bit ahead of themselves. In addition, we are coming off a mid-term election, which has historically been good news for markets. According to Ned Davis Res

How We Help Protect Your Portfolio in a Market Pullback

What Happened in the Markets This Past Week? After a period of historic market tranquility in 2017, a few weeks ago we reallocated and rebalanced our portfolios in order to provide greater opportunities and to help reduce risk going forward into 2018. With the rapidly changing market conditions of the last week, it’s more important than ever to be sure you are diversified, and properly balanced and allocated. Because we took a pro-active approach to managing our clients' accounts, they are in a better position to weather the volatility that has been generally absent from the markets for the past year. On Monday, February 5th, the S&P 500 Index and Dow Jones Industrial Average (DJIA) both fell more than 4%, marking the worst one-day percentage decline since August 2011. When combined with declines from last Friday, the last two trading sessions resulted in these indices falling more than 6%, bringing the indices back to levels as of mid-December 2017. Remarkably, the recent sell-off ends a streak of more than 400 trading sessions since the last time the S&P 500 Index had experienced a 5% pullback (dating back to the Brexit vote of June 2016). Asset Class Index January Return February Return (through Feb 5th) YTD-2018 Return (through Feb 5th) U.S. Large Cap S&P 500 5.7% -6.1% -0.8% U.S. Large Cap Dow Jones Ind Avg 5.8% -6.9% -1.5% U.S. Small

![]()

Terms and Conditions | Privacy Policy | Disclosures

Case studies are intended to illustrate the types of financial issues faced by actual clients. They should not be construed as a testimonial for or endorsement of Lineweaver Wealth Advisors. They do not represent the experience of any advisory client. Each client’s situation is different, and their goals may not always be achieved. Lineweaver Wealth Advisors, LLC, is not engaged in the practice of law or accounting. Tax information provided is general in nature and should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation. Tax rules and regulations are subject to change at any time.

Crain's Cleveland Business is a print and online newspaper delivering local business news and information to Cleveland's business executives, which is published by Crain Communications Inc. The Crain's 2024 list may employ different methodology than described above for similar designations granted in other years. No clients were consulted and no fees were paid to determine the winners; the award is based on assets under management. Neither the participating candidates nor their employees pay a fee in exchange for inclusion on Crain's 2024 List. However, recipients may pay a fee to Crain, an affiliate, or an unaffiliated third party in exchange for plaques or article reprints commemorating the designation. The publication should not be construed by a client or prospective client as a guarantee that they will experience a certain level of results if the recipient is engaged, or continues to be engaged, to provide investment advisory services; and should not be construed as a current or past endorsement of the recipient by any of its clients. Lineweaver Wealth Advisors was ranked in the Top 25 of Crain’s of Cleveland’s annual list of Registered Investment Advisors. The award is based on assets under management in the years 2024. In 2023, Lineweaver Wealth Advisors was ranked in the Top 15 of Crain’s of Cleveland’s annual list of Registered Investment Advisors. The award is based on assets under management in the years 2023. In 2021 and 2022, Lineweaver Wealth Advisors was ranked in the Top 20 of Crain’s of Cleveland’s annual list of Registered Investment Advisors. The award is based on assets under management in the years 2021 and 2022 respectively.

Nominees in the Top 100 Magazine selections are not required to pay a fee for consideration. Individuals appearing in half and full page editorials, have paid a fee for additional exposure. Candidates for consideration are selected utilizing proprietary software. Top 100 Magazine analyzes the results before making their final selections. Financial Professionals and/or wealth managers must also met the following criteria; 1. Be registered with the SEC as a registered investment advisor or a registered investment advisor representative; 2. Have no more than 1 filed complaint with a regulatory agency; 3.Never been convicted of a felony. Third-party rankings and recognitions are no guarantee of future investment success and do not ensure that a client or prospective client will experience a higher level of performance or results. These ratings should not be construed as an endorsement of the Financial Professional by any client nor are they representative of any one client's evaluation. Participants for the Top 100 in Finance appearance were reviewed in 2022, and recognized in March of 2023. Lineweaver Financial Group appeared in Money magazine in 2015, Fortune Magazine in 2016, WTAM 1100 in 2018, Forbes in 2020, Channel 5 in 2020, and Top 100 in Finance in 2023.

Lineweaver Financial Group ©

Powered by  Virteom

Virteom